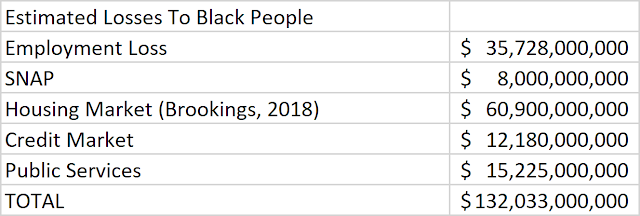

Economic Insecurity:

A federal government default would trigger an economic crisis with severe ramifications for all Americans. However, Black communities are more likely to face higher levels of economic insecurity due to existing disparities. Historically, Blacks have faced barriers in wealth accumulation, employment discrimination, and access to quality education. These factors already contribute to higher poverty rates and lower median household income in the Black community. A default would further exacerbate these challenges, causing increased unemployment, reduced social safety net benefits, and diminished economic opportunities, widening the wealth gap and stifling progress toward economic equality. The dollar losses alone would total $15 billion.

The housing market is a fundamental pillar of financial stability for many families. A federal default could lead to a significant downturn, leading to a decline in property values, an increase in foreclosures, and a contraction of lending activities. Black Americans, who historically have faced discrimination in housing and mortgage lending, are likely to experience more pronounced hardships. They would confront challenges in maintaining homeownership, face difficulties in accessing affordable rental properties, and witness the erosion of already limited housing equity. Consequently, a federal default could contribute to heightened housing insecurity, housing instability, and potential displacement within Black communities. Housing impacts might total a negative $60 billion, due to an increase in foreclosures and unethical behaviour on the part of housing market participants.

Access to Credit and Lending:

In times of economic turmoil, access to credit and lending becomes crucial for individuals and small businesses. Unfortunately, Black Americans have encountered discriminatory lending practices, making it more difficult to obtain loans, secure capital, or start businesses. A federal government default could exacerbate this situation as financial institutions become more risk-averse and tighten lending standards. Consequently, Black entrepreneurs and aspiring business owners would face even greater hurdles in securing funding, hindering their ability to create jobs, generate wealth, and contribute to the economic recovery. Under a default scenario, we expect banks to increase interest rates, issue fewer credit cards, and lower credit limits and lines for credit for outstanding cards.This might total a $12.1 billion dollar loss.

Disproportionate Impact on Public Services:

Government programs play a vital role in providing essential services to vulnerable communities. A federal government default would likely lead to budget cuts, reduced funding for social programs, and increased austerity measures. This would disproportionately affect Black Americans, who rely heavily on public services such as Medicaid, SNAP (Supplemental Nutrition Assistance Program), and affordable healthcare. The erosion of these vital programs would undermine healthcare access, exacerbate health disparities, and deepen the existing social and economic inequalities faced by Black communities. Lost SNAP benefits would total $6 billion. Other public service losses would total $15 billion.

Summary

A federal government default would have dire consequences for all Americans, but given systemic inequities and historical disadvantages, Black Americans would bear a disproportionate share of the burden. It is crucial for policymakers to prioritize proactive measures to protect marginalized communities during times of economic stress. These measures might include targeted investment in housing and job creation, equitable access to credit, housing assistance, and safeguarding essential public services. By recognizing and addressing the potential impact of a federal government default on Black people, we can strive towards a more inclusive and resilient society that ensures economic and social justice for all.